Chat with AGB Board Bot

Chat with AGB Board Bot

Opinions expressed in AGB blogs are those of the authors and not necessarily those of the institutions that employ them or of AGB.

The NACUBO-Commonfund Study of Endowments® (NCSE) has shown over the years that operating budgets are claiming a greater share of annual endowment spending. That trend continued in the 2025 study, released in February 2026. Is the most recent jump an anomaly or the new normal?

The purpose of an endowment is to provide financial support such that it enables the endowed institution to pursue its mission in perpetuity. There are many corollary purposes (and benefits) associated with endowments, one of which is the opposite of perpetual, and that is funding operating expenses on a day-in, day-out basis—in other words, the annual operating budgets that keep the place running.

Endowments provide colleges and universities with a dependable, long term source of financial support—one that helps buffer the institution from volatility in enrollment, gift revenue, and state or federal appropriations. Because an institution’s credit rating is closely linked to the consistency of these funding streams, a stable endowment contributes directly to its overall financial strength. This stability is essential for sustaining academic programs and mission critical initiatives that cannot be paused, scaled back, or compromised due to short term fluctuations in operating resources, even when those activities fall outside the annual budget.

Although there are some notable exceptions, especially among the largest endowments, institutions whose endowment payout is a relatively small percentage of the operating budget can generally take on more equity risk in their portfolio, as a severe short-term to medium-term decline is less likely to disproportionately impact the institution’s operating needs. Conversely, institutions that rely more heavily on their endowment to fund their operational costs should carefully evaluate the amount of portfolio risk they can take on to protect against large cuts in the operating budget should there be a sharp decline in equity markets.

NCSE data for fiscal year (FY) 2024 and FY 2025 show a marked jump in the share of endowment spending earmarked for operating budget support. The question is whether two years’ data are an aberration or a new normal. Data reported several decades ago may provide the answer to that question.

Long-term trends suggest that colleges and universities have become increasingly reliant on their endowment to fund annual operating budgets as measured by the share of their budget that the endowment funds. In the late 1970s, the average was just above 4.0 percent, while the median hovered around 3.0 percent. In the following years, the rate grew, reaching an average of 4.4 percent for FY 1982 and FY 1983 (median data are not available for this period). The study did not examine endowment support for the operating budget for a number of years; two metrics used at times during this period were endowment assets per full-time student and per full-time faculty member.

The study resumed inquiring about the share of operating budget supported by endowment for FY 2008. That year, participating institutions reported that an average of 10.5 percent of their budget was supported by endowment—more than twice what it was nearly 25 years earlier. The very next year, the average support level increased markedly—to an average of 13.4 percent. In FY 2010, the support level returned to the 10.5 percent reported two years earlier.

FY 2018: A Departure Point

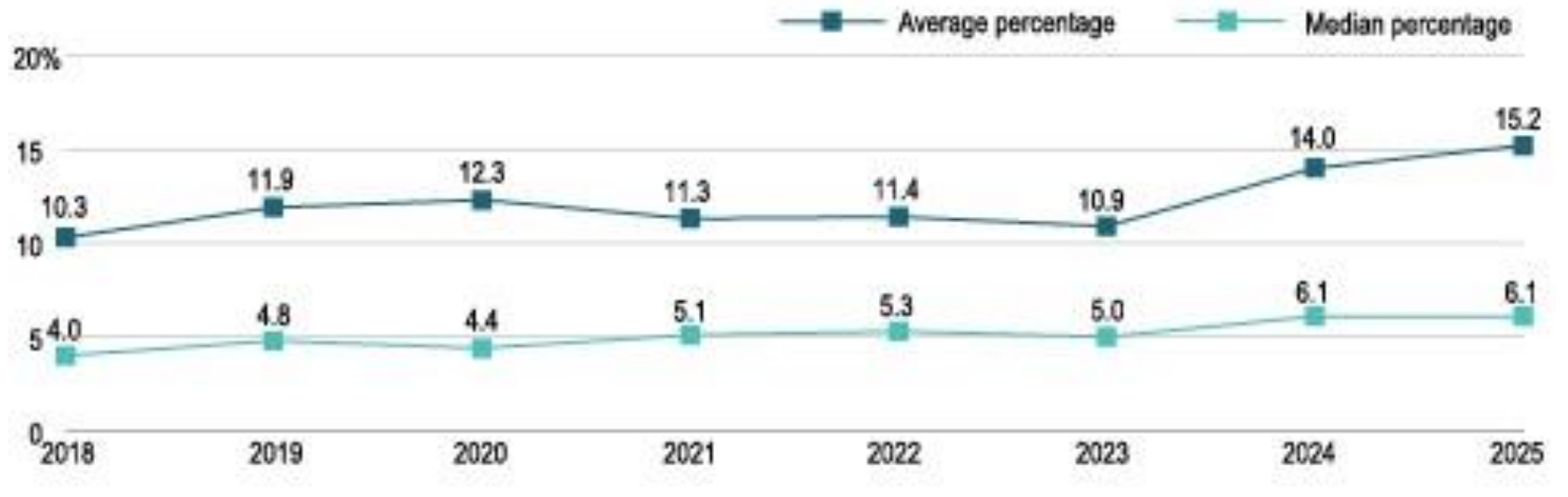

For the next seven fiscal years, average support levels returned to single digits, ranging from a low of 7.9 percent (FY 2017) to highs of 9.7 percent (FY 2015 and FY 2016) while averaging 9.0 percent annually. In FY 2018, the double-digit threshold was crossed once again, and it has increased from there as the graph below shows. From FY 2018 to FY 2019, there was a 15.5 percent year-over-year increase. Although the increase was moderate in FY 2020, it nonetheless breached the 12.0 percent level. From FY 2023 to FY 2024, the share of the operating budget supported by endowment once again showed a sharp rise—28.4 percent year over year. For FY 2025, it jumped more than one full percentage point and set a new high by topping 15.0 percent. In other words, the past three fiscal years alone have seen an increase of nearly 40 percent.

Percentage of Operating Budget supported by endowment FY 2018–FY 2025

Of course, outlying data points can heavily influence the average, in this case a relatively few institutions that may have implemented sharply higher levels of spending. But the median data for the same period (FY 2018–FY 2025) are not out of line with the average. The rise from FY 2018’s median 4.0 percent to 6.1 percent for FY 2024 and FY 2025 is half again as much; further, that 4.0 percent median in FY 2018 was never as low again.

Segmenting Data by Size of Institution

The study data above are aggregated values for all participating institutions. What happens when data are segmented by endowment size? Historically, institutions with larger endowments have had a greater proportion of their operating budgets supported by endowment spending. That was true in FY 2025, as institutions with assets between $1 billion and $5 billion relied on endowment to support 20.1 percent of their operating budgets; institutions with assets over $1 billion spent at an 18.1 percent rate. Both segments with assets under $100 million supported 14.8 percent of their budgets through their endowments; segments with assets between $101 million and $250 million were the least reliant, spending 12.1 percent of their endowment funding to support their operating budgets.

Looking at the multiyear period from FY 2018 to FY 2025 examined earlier in this blog post, perhaps the most significant observation is the differing rate of spending growth between institutions comprising the largest and smallest size segments.i Here, the increase in operating budget support has been greater among institutions in the smaller segment. Among this size segment, the average percentage of the operating budget supported by endowment more than doubled (from 6.9 percent to 14.8 percent) over the period. Institutions with the largest endowments (over $5 billion) increased their rate of support as well, but by far less, as it rose from 16.7 percent to 18.1 percent, respectively, at the beginning and end of the period. (It did, however, rise into the 19 percent range on three occasions.)

Another way to view the data is through the relative starting and ending points for the two segments: In FY 2018, institutions at the smaller end of the size spectrum supported an average of 6.9 percent of their operating budget through endowment versus 16.7 percent of the budget supported by institutions at the opposite end. By FY 2025, the levels of support were 14.8 percent and 18.1 percent, respectively. In other words, a gap of 9.8 percentage points at the beginning had narrowed to 3.3 percentage points at the close of the period.

Sorting Data by Type of Institution

The study also segments participating institutions by type; here, the differences among segments were not as great as they were when measured in terms of size. There were patterns, however: 1) with one exception, from FY 2018 through FY 2025, private institution endowments supported a greater share of the operating budget than did the endowments of public institutions; 2) public institutions and institutionally related foundations (IRFs) showed a marked increase in endowment support for the budget in FY 2025; and 3) IRFs showed the greatest year-to-year variability in endowment support for the budget.

Private institutions funded an average of 11.0 percent of their annual operating budgets from their endowments from FY 2018 to FY 2025. Over the same period, public institutions averaged 7.5 percent—a lower percentage, but it is important to note that this results in large part from the support they receive from state governments. Private institutions’ funding levels were in double digits for seven of the eight years, while for public institutions, only one—FY 2025—had a double-digit funding level, soaring to 13.1 percent from 8.4 percent in FY 2024. IRF support levels were volatile: an average of 24.7 percent in FY 2025, 19.4 percent in FY 2024, 13.4 percent in FY 2022, 19.8 percent in FY 2020, and 20.6 percent in FY 2019 interspersed with 9.6 percent in FY 2023, 8.6 percent in FY 2021, and 8.1 percent in FY 2018. That said, in many of the years when average IRF support levels were highest, the median levels ranged between 1.0 and 2.0 percent, indicating very high levels of budget support from a limited number of IRFs. (The same disparity between average and median levels was evident among public institutions as well, but not among private institutions where the disparity was much less.)

Impact of Significant External Events

The data do not appear to indicate a strong link between major economic or societal events of the period beginning in 2008 when the study reintroduced a related question. An example is the financial crisis and Great Recession of 2007-2009. The draw on endowment to support the operating budget appears to have risen sharply in just one of those years, FY 2009, when it hit 13.4 percent. This was higher than the 10.5 percent draw in the adjacent FY 2008 and FY 2010. It’s possible that institutions fell back on other sources of income, such as tuition and fees, to temporarily temper the loss in endowment values that accompanied the crisis. The COVID-19 pandemic does not seem to have had a major effect. Based on a fiscal year calendar, 2021 should have been the year of greatest impact; yet the share of endowment support for the operating budget declined to 11.3 percent in FY 2021 from 12.3 percent in FY 2020 and increased by just one-tenth of a percentage point in FY 2022.

Conclusion

The NACUBO-Commonfund data show that among the 657 respondents to the 2025 study, endowments are supporting an ever-greater share of the annual operating budget. In recent years, the share of the operating budget supported by the endowment has spiked, but the trend has been upward for many years. The reason behind this trend is less clear.

In recent years, investment returns have been good, meaning that, for the most part, endowments have grown larger. But the 2025 study shows that 10-year returns averaged 7.7 percent for all study participants and—harking back to the reference to perpetuity at the beginning of this discussion—an annual average of just 6.2 percent since the beginning of this century. That isn’t likely to cover inflation, management fees, and—the topic here—the operating budget (much less all the other demands on spending from endowment).

Further, data show that institutions at the smaller end of the endowment size spectrum are growing the share of their operating budget funded by endowment at a much faster rate than their larger counterparts. Reference the point made earlier that in FY 2025 the respective levels of support were 14.8 percent and 18.1 percent for endowments with assets under $50 million and those with assets over $5 billion. A steep or protracted retrenchment in the financial markets would hurt all endowments, but institutions with larger asset pools are likely to better withstand it.

Finally, inflation has reemerged as a significant challenge for higher education. After a subdued decade following the financial crisis, both the Higher Education Price Index (HEPI) and the Consumer Price Index (CPI) have shown notable increases. In FY 2025, HEPI rose to 3.6 percent (up from 3.4 percent in FY 2024), while CPI reached 2.6 percent (down from 3.3 percent in FY 2024). HEPI has consistently outpaced CPI, exceeding it in nine of the past eleven years, and has averaged 3.8 percent annually over the last five years. This persistent rise in HEPI underscores that colleges and universities are facing the mounting pressure of higher operating costs.

While some stabilization or “evening off” may occur if inflation moderates and institutions adjust their cost structures, long-term financial pressure is expected to remain. These institutions will need to balance growing operational needs with responsible endowment spending to protect long-term sustainability and intergenerational equity.

Read the press release here or request a copy of the full 2025 NACUBO-Commonfund Study of Endowments here.

Amanda Novello is a senior policy and research analyst at Commonfund Institute.

With Thanks to AGB Mission Champion: Commonfund

![]()