Chat with AGB Board Bot

Chat with AGB Board BotNavigate your strategic options.

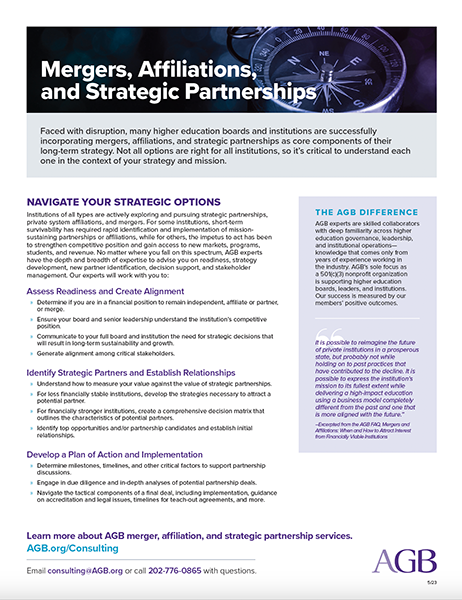

Faced with disruption, many higher education boards and institutions are successfully incorporating mergers, affiliations, and strategic partnerships as core components of their long-term strategy. Not all options are right for all institutions, so it’s critical to understand each one in the context of your strategy and mission.

Recommended resources.

Higher Education Business Models Under Stress

Podcast

with Chris Moloney, Melody Rośe, and Larry D. Large

Questions for boards.

Click below to reveal key questions for your board to consider.

Strategy

-

- How can we determine if we are in a position to merge, affiliate, consolidate, or remain independent?

- How can we ensure that the board and senior leadership understand our institution’s competitive position?

- What is the best way to build alignment among our critical stakeholders?

- How should we measure our value against the value of strategic partnerships?

- What are the best approaches to developing strategies to attract a potential partner?

Processes

-

- What attributes and characteristics should be a part a decision matrix?

- How do we approach identifying opportunities and/or partnership candidates, and establishing initial relationships?

- What are the appropriate milestones, timelines, and other critical factors that should support partnership discussions?

- What should be part of the due diligence of a potential merger, affiliation, or strategic partnership discussion?

- Who manages the tactical components of a final deal, such as implementation, accreditation guidance, legal issues, and faculty agreements?

AGB helps you deliver long-term prosperity.

AGB’s Mergers, Affiliations, and Strategic Partnership practice area is exclusively focused on supporting positive outcomes for our members. AGB experts are skilled collaborators with deep familiarity across higher education governance, leadership, and institutional operations—knowledge that comes only from years of experience working in the industry. Let us work with you to:

Assess readiness and create alignment.

- Communicate and educate the board and senior leadership on challenges and opportunities.

- Determine your financial position.

- For a merger or affiliation, identify if you are on the buy side or sell side.

- Create a communications plan to generate alignment among critical stakeholders.

Identify strategic partners and establish relationships.

- Calculate your prosperity gap.

- Understand the quality of earnings.

- Create a board subcommittee to discreetly begin exploring options and alternatives.

- Develop a decision matrix to evaluate the attributes and characteristics of potential partners.

Develop an action and implementation plan.

- Establish realistic milestones and timelines.

- Engage in due diligence and in-depth analyses.

- Oversee the tactical components of a final deal.

The business model for higher education is under severe stress.

Making decisions on long-term strategy—such as how and when to establish a build, buy, affiliate, or partner strategy—is critical to mitigating risk and enhancing competitiveness. AGB experts have the depth and breadth of expertise to advise you on readiness, strategy development, new partner identification, decision support, and stakeholder management.

Contact AGB.

To learn how AGB Consulting’s assessment and development services can benefit your institution, please contact 202-776-0865 or [email protected]. Or use this contact form: